How to Implement the Systematic Shortlist: Basket-Portfolio

Higher returns (+11.82% alpha) and lower market sensitivity (0.89 beta)

To read my full disclaimer click here.

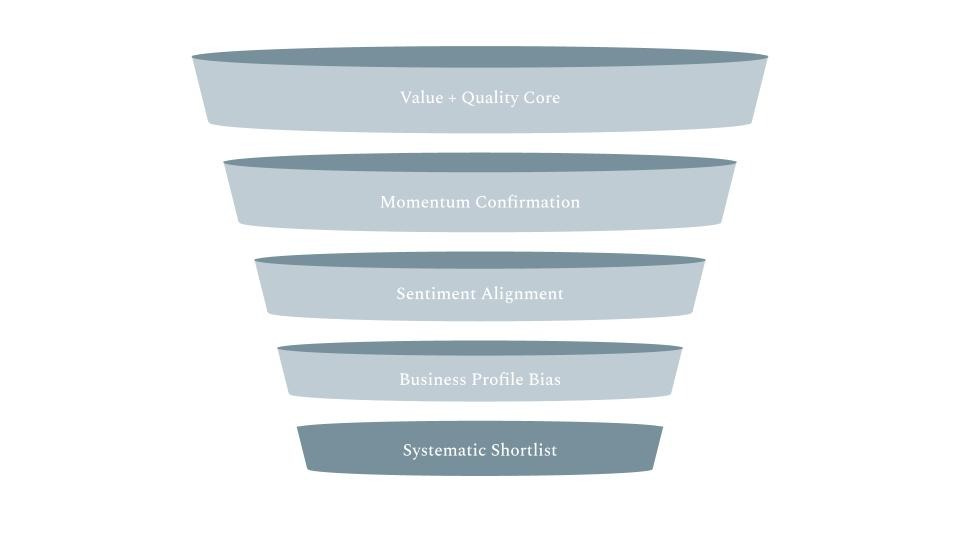

The Systematic Shortlist

The Systematic Shortlist is built to be boring in the best way. Every company has to clear four independent filters because it forces overlap: when value, quality, and trend all agree, the “why” stops being a debate and starts being a rules-based decision.

1) Value + Quality Core

The shortlist sorts the investable universe to find good businesses selling at good prices. In practice, that means combining a quality metric (returns on capital) with a cheapness metric (earnings yield).

2) Momentum Confirmation

Being cheap and good is not enough if the market still expects things to get worse. Momentum makes the shortlist prove the business is improving and the market is aware of it.

3) Sentiment Alignment

The shortlist favors setups where the big inputs such as valuation, earnings revisions, price action, and insider behavior push in the same direction instead of fighting each other.

4) Business Profile Bias

All else equal, the shortlist leans toward companies that can fund themselves, reinvest at high returns, and keep those returns high: Cash Cows and Stars.

How to Implement the Systematic Shortlist: Basket-Portfolio (“Build Your Own ETF”)

Instead of building a portfolio over time by adding a few companies periodically, you can use a basket. In the first method, you try to keep each stock about the same size, adjust once a year, and reinvest. The basket plan turns the shortlist into one new basket each month, like your own ETF. You buy an equally weighted basket, hold it for 12 months, then reinvest it.

How it works (monthly cadence)

Once per month (e.g., first week): pick 20+ names from the current shortlist and build a new equal-weight basket. Record the start date.

Buy in one shot: treat the basket like a single “mini-fund.” Fractional shares are fine.

Hold ~12 months: no tinkering. Let the system do what it does.

Tax-aware exit: near the one-year mark, you can realize losses slightly early and hold winners a few days beyond one year for long-term treatment, then close and reinvest into the newest basket.

Repeat forever: after month 12, you’re always running ~12 baskets in parallel with one added each month, one closed each month.

Two details that keep it clean

Names can repeat across months. If a stock still qualifies, it can show up in more than one monthly basket. Your position grows as long as the company stays strong.

It feels like an ETF, but you still own the underlying securities directly.

Note: Many brokerages now offer basket tools that make setup and rebalancing easier.

Systematic Shortlist Results (Shortlist Index)

The Shortlist Index page tracks the Systematic Shortlist over time. Each edition is generated using the same rules-based framework and published on a fixed cadence. The goal is to apply a consistent process and observe how cohorts evolve as the underlying businesses compound.

As of 1/28/26, the average across all cohorts shows:

Return: +11.82% above the S&P 500

0.89 average beta

Higher return with lower market sensitivity across cohort averages.

**Future versions could scale the same system worldwide - create a shortlist for each country or region.

The Development of the Systematic Shortlist

I started with Joel Greenblatt’s Magic Formula because it shows a simple truth, that value plus quality can work when the rules stay fixed. The core is mechanical: begin with a defined universe (e.g. 3,500 tradable U.S. stocks), rank companies by Return on Capital and Earnings Yield, combine the ranks, and focus on the overlap.

But “cheap” can stay cheap for a long time, so I kept the top quartile and added three filters. Filter 1 looks for the trend to turn up. Filter 2 wants signals (e.g. valuation, earnings revisions) to agree instead of fight. Filter 3 tilts toward Cash Cows and Stars that can fund growth and keep returns high.

Joel Greenblatt and Magic Formula Investing

Greenblatt’s Magic Formula is a simple idea: buy good companies when they’re cheap systematically, not emotionally. Start with a defined universe ranked by Return on Capital and Earnings Yield, combine the ranks, and focus on the best blend of quality and cheap.

Key Takeaway: it’s not trying to buy the “best business” at any price, or the “cheapest stock” regardless of quality. It’s explicitly hunting the overlap.

Risks (the real one is time)

Greenblatt is blunt - the Magic Formula can underperform for years even if it works over a full cycle. Most people quit after “a year or two” of lagging. His guidance is that if you aren’t willing to run it for a minimum of three to five years, you’ll likely abandon it before it has a chance to work.

There’s also a structural risk: the formula ranks using past earnings, which can make “cheap” look cheap for the wrong reason if earnings are temporarily inflated (or about to fall).

Results (as shown in Greenblatt’s tables)

Magic Formula at 30.8% vs 12.4% for the S&P 500 over the period (1988–2004).

For the largest 1,000 stocks: 22.9% vs 12.4% for the S&P 500 over the same period shown.

Key takeaway: value + quality work but the ride can be tough enough to shake out most people.

Momentum Theory (Jagadeesh & Titman)

Momentum is the idea that winners tend to keep winning (for a while), and losers tend to keep losing. Jagadeesh & Titman (1993) document that buying recent winners and selling recent losers generated significant positive returns over 3 to 12 month holding periods.

That’s why momentum belongs inside the shortlist: value and quality tells you what should be attractive and momentum helps tell you whether the market is starting to agree. Momentum is a confirmation filter, not a replacement for valuation discipline.

Business Profile Bias (Cash Cows and Stars)

This filter favors compounders with Richard Koch’s use of growth-share categories (cash cows, stars, question marks, dogs) as a practical way to classify business situations and opportunity.

Cash Cows: low growth but highly profitable; a market leader that throws off cash. In shortlist terms, these businesses can self-fund, buy back stock, pay down debt, or selectively reinvest without needing perfect capital markets.

Stars: a leader in a high-growth market, with the potential to be (or become) very profitable. In shortlist terms, reinvestment can compound because the runway is long and the leader’s unit economics are advantaged.

Why the bias exists: the biggest winners tend to come from a small subset of businesses and outcomes (Koch frames this as an 80/20 pattern). So the shortlist tilts toward leaders, self-funded models, and high-return reinvestment without pretending turnarounds and cyclicals don’t exist.

Bottom Line

The Systematic Shortlist is meant to be boring in the best way.

First, it looks for good businesses at good prices by pairing returns on capital with earnings yield.

Then it makes the idea earn its spot with momentum, so “cheap and good” also has a turning trend.

Next, it looks for alignment across big signals like valuation, earnings revisions, price action, and insider behavior, so the setup is not fighting itself.

Finally, it leans toward Cash Cows and Stars that can fund themselves and keep high returns over time.

The simplest way to run it is the basket method: buy an equal-weight group once a month, hold 12 months, and then reinvest.

Want To Follow Along?

The Systematic Shortlist is published every Monday.

Free subscribers get the weekly sector breakdown showing where value, quality, and momentum are converging.

Paid subscribers receive full access to the list of company names.